Most people think geopolitical conflict is something that happens “over there.”

A missile strike. A naval standoff. A tense headline about the Strait of Hormuz. It feels distant. Strategic. Political.

But in insurance, distance is an illusion.

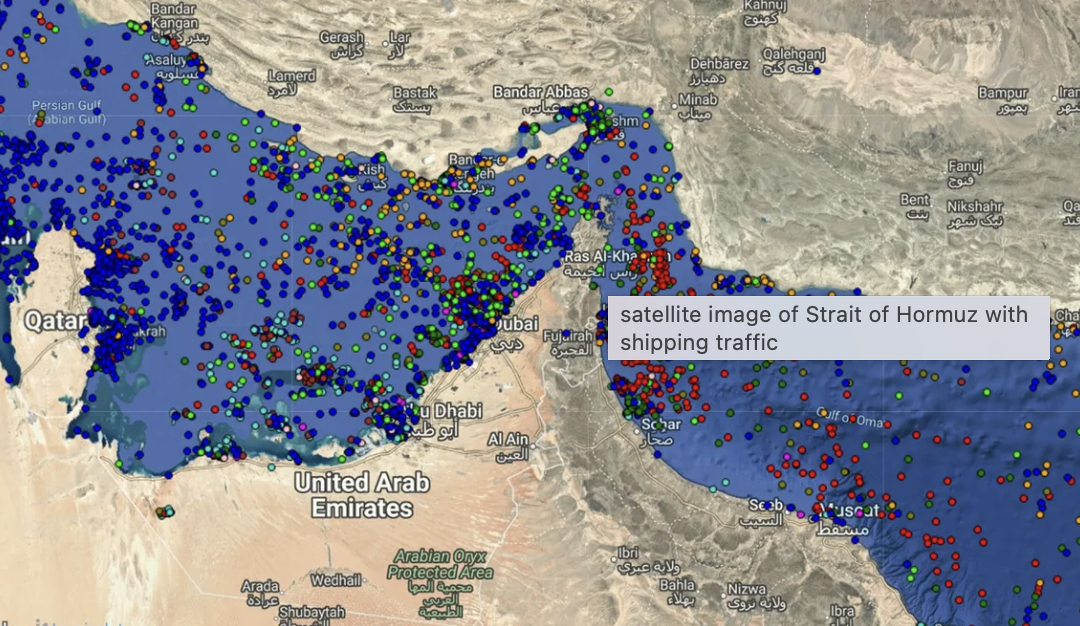

When tensions rise in the Strait of Hormuz, one of the most important shipping lanes in the world, the first reaction does not come from politicians. It comes from underwriters.

Nearly twenty percent of the world’s oil flows through that narrow corridor. When military activity escalates in that region, marine war risk insurers immediately reassess exposure. Premiums move. Cancellation notices can be issued. Coverage terms tighten. Underwriters begin recalculating aggregation risk.

There may not always be dramatic public press releases from the Lloyd’s market or the Joint War Committee, but that does not mean nothing is happening. The insurance market adjusts quietly and quickly. War risk premiums increase. Voyage pricing changes. Reinsurers begin modeling worst case scenarios.

That is where the real story begins.

If hull and cargo coverage becomes more expensive for oil tankers transiting the Gulf, the cost of energy transportation rises. Higher transportation cost contributes to higher energy prices. Higher energy prices increase insured values. Replacement costs climb. Inflationary pressure builds.

And once inflation builds, every line of insurance feels it.

Commercial property. Residential homeowners. Auto. Builders risk. Inland marine. It all connects.

If reinsurers take on elevated marine war exposure, their capital is stressed. When capital is stressed, pricing discipline follows. Reinsurance renewals harden. Primary carriers adjust rates. Deductibles rise. Capacity tightens.

A conflict thousands of miles away can quietly filter into the renewal notice of a homeowner in Florida or a strip center owner in Texas.

Insurance is global capital at work. It does not recognize political borders. It responds to risk.

This is why conflicts are never isolated events from an insurance perspective. They are systemic stress tests.

It is also why the language around “declared war” versus “authorized force” matters less to insurers than exposure reality. Whether a conflict is formally declared or simply authorized through congressional resolution, the market responds to probability of loss, not terminology.

We have seen this pattern before. War risk zones are reclassified. Premiums spike for specific transits. Underwriters demand additional information. Governments sometimes step in with backstops. Then markets stabilize, or they do not.

The important point is this. No matter how the situation evolves, the ripple effects will be felt broadly.

Energy markets move first. Insurance markets move second. Consumers feel it third.

Even people who have never heard of marine hull insurance will ultimately be affected if geopolitical instability pushes capital costs higher.

This is why understanding global risk matters even for a local insurance agency. The pricing of a homeowner’s policy in Florida is not determined solely by hurricanes. It is influenced by global reinsurance capacity, inflation, energy costs, and geopolitical stability.

When countries engage militarily in complex regions, even with strategic intentions, there are always downstream economic effects. Responsible risk management means thinking beyond the immediate headline and understanding the capital impact that follows.

As of now, the insurance market is recalibrating. War risk pricing in the Gulf is adjusting. Underwriters are reassessing exposure. The Joint War Committee and major marine markets are being watched closely.

We will continue monitoring developments carefully.

Because in insurance, what happens in a narrow strait halfway around the world can eventually show up in your renewal notice.

And that is not politics. That is risk.